Friday May 17 2024 15:49

7 min

Stock markets have retreated a bit after a good run to record highs. We have had a slew of all-time highs for stock markets this year and we got fresh peaks in the wake of the US inflation report.

BofA says fund managers are the most bullish on stocks since November 2021. That’s shown up in a fresh all-time high for the S&P 500, Nasdaq and MSCI All-Country World Index, among others.

This week the FTSE 100 notched its 12th all-time high close in a month, matching a record for the index. London and European stock markets closed lower on Thursday, breaking a nine-day win streak, and are tending to the downside for the moment in early trade on Friday with the dollar firmer for a second day.

Сalculate your hypothetical P/L (aggregated cost and charges) if you had opened a trade today.

Market

Instrument

Account Type

Direction

Quantity

Amount must be equal or higher than

Amount should be less than

Amount should be a multiple of the minimum lots increment

USD

EUR

GBP

CAD

AUD

CHF

ZAR

MXN

JPY

Value

Commission

Spread

Leverage

Conversion Fee

Required Margin

Overnight Swaps

Past performance is not a reliable indicator of future results.

All positions on instruments denominated in a currency that is different from your account currency, will be subject to a conversion fee at the position exit as well.

The Dow Jones index closed slightly lower for the session after briefly hitting 40,000 for the first time as Walmart shares jumped.

It largely looks like a meaningless round number for a badly-composed index — Wall Street analysts noted the Dow Jones index had a “relevance” problem as recently as March. Five stocks (MSFT, CAT, GS, CRM, APX) have made up half its gains from 30,000 but that may still be significant. Here’s BofA:

“ The soft-landing scenario is unfolding [...] we think a [ten-year yield] decline from 4.35% to the 3.25% area in the next 6-12 months is a good possibility — and likely non-consensus.”

Cyclical bull market but it has run up a lot recently and looks heavily overbought — it may need a break soon.

It’s been one of those weeks. Meme stocks made a comeback this week but, like a striking match, fizzled almost as quickly as the mania began. GME shares cratered by another 30% yesterday as the wind came out of the movement.

Still, the shares are up a lot for the week. Roaring Kitty keeps posting cryptic messages. More importantly, global stock markets reached fresh record highs. It was perhaps important that they notched these before the cooler-than-expected US CPI inflation number — and kicked on some in its wake.

This week has seen some moves in commodities — copper prices reached all-time highs above $5 a pound amid a huge arb trade between London and NY, platinum broke out to its highest in a year and silver tested $30.

Orange juice futures hit a record high. Extreme volatility in cocoa continued as prices plunged 19% in a day, the biggest drop in decades. Meanwhile, data showed China sold a record amount of Treasury and US agency bonds to buy gold in the first quarter.

Stock markets liked the fact that the CPI could have been worse. But it was a mixed picture. The US CPI inflation print for April marked the first cooling in several months, with the headline print down to 3.4% from 3.5%. Core CPI inflation slowed 20bps to 3.6%, its lowest level since April 2021, with the month-over-month down to 0.3% after three months at 0.4%.

Disinflation returns:

Supercore CPI (core services less housing) declined to +0.42% MoM in April vs +0.65% prior. Whilst it was the slowest monthly increase since December, recent monthly gains mean the annual rate of supercore inflation rose to 4.9%, the highest in a year.

This remains way too high for the Fed to cut next month. And services inflation remains very sticky and accounts for almost all of the headline CPI.

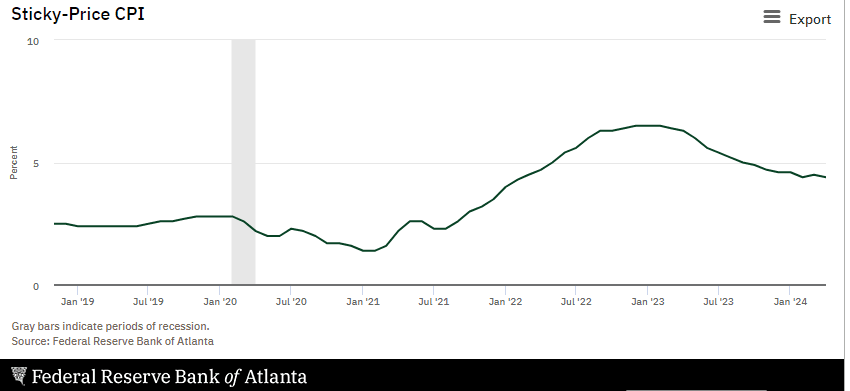

Another measure, the Atlanta Fed's sticky-price consumer price index (CPI) — a weighted basket of items that change price relatively slowly — increased 4.6 per cent (on an annualised basis) in April, following a 5.0 per cent increase in March.

Whether the Fed has any say over these CPI prints is another matter entirely… a few tenths of a per cent here or there is kind of meaningless – we are at 3-4% reality for inflation for a long time.

The Fed will accept this – as said many times before – tacitly at first (as it’s doing now) and then explicitly. That’s because we are entering an era of instability that will require ever-larger deficits to finance promises at home and abroad. Cuts are in the mail, even if supercore says “not in June”.

US 10yr and 2-year yields dipped to their lowest level in a month and a half as markets moved to price at a faster pace of Fed cuts this year, with 50bps of cuts now priced. The gold price rallied to its highest point in a month as yields ticked down and the dollar hit its weakest point in a month before rallying on Thursday and Friday. Silver broke out to test $30.

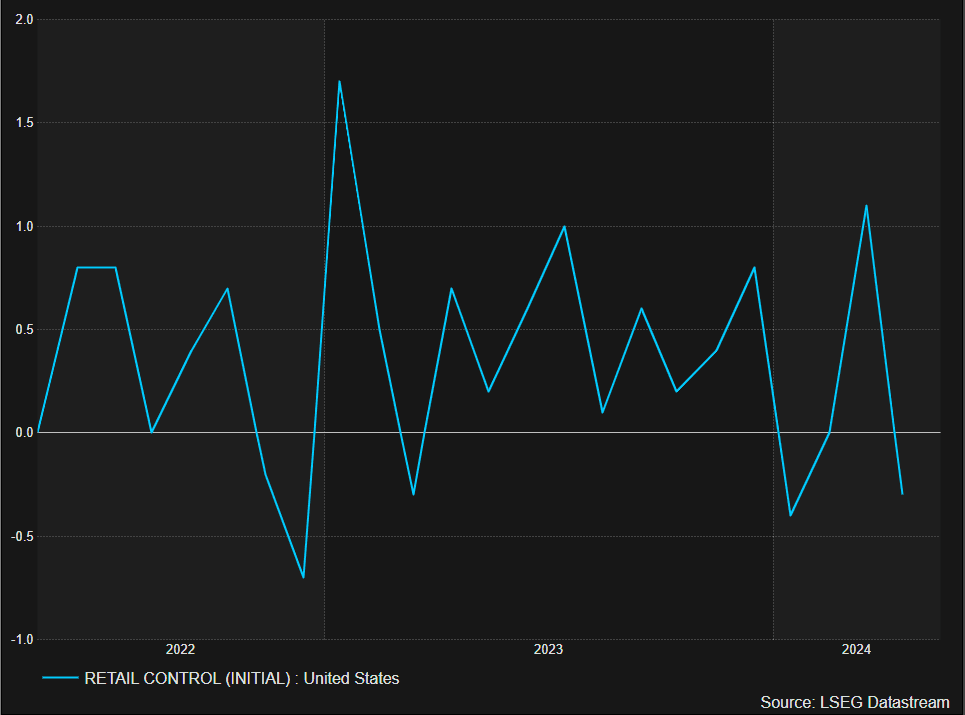

Amid the marginally softer-than-expected CPI data, we saw some weakness in the data elsewhere – the Empire State Manufacturing Survey was bad and the retail sales control group declined 0.3%. There is a sense that consumer spending proxies are rolling over.

Whilst US CPI was down, if we see the consumer rollover quickly, we could be left with a more stagflationary environment. The Fed will have to accept inflation is going to be higher for longer soon enough as we move from the tacit to the explicit.

I should note what BofA says though: “Stagflation was so 2022 ... In our view, the key risk to watch is re-acceleration in (services) demand, not ‘stagflation.’”

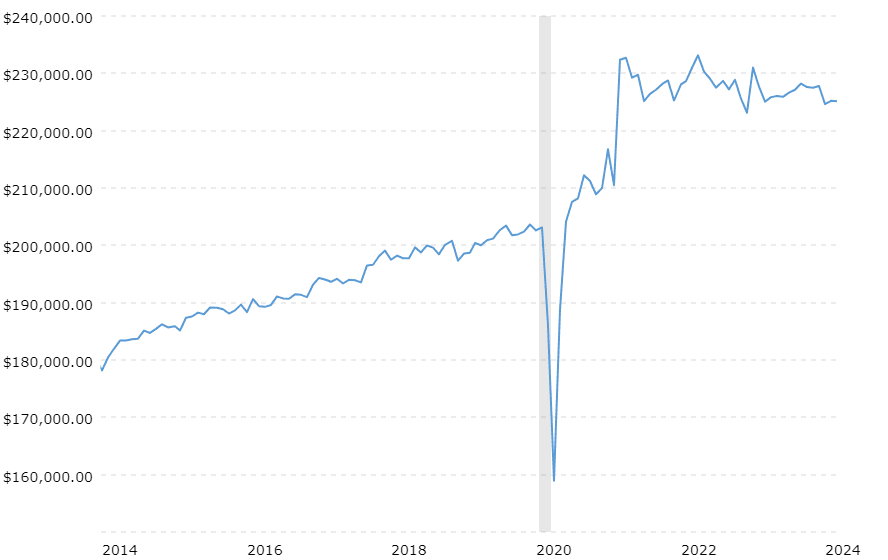

Retail sales indicate the US consumer starting to falter:

Adjusted for inflation, retail sales have struggled for a while — the chart from Macrotrends below shows US total real (inflation-adjusted) retail and food service sales.

When considering shares, indices, forex (foreign exchange) and commodities for trading and price predictions, remember that trading CFDs involves a significant degree of risk and could result in capital loss.

Past performance is not indicative of any future results. This information is provided for informative purposes only and should not be construed to be investment advice.

Tags Directory

View allLatest

View all

Thursday, 19 December 2024

5 min

Thursday, 19 December 2024

3 min

Wednesday, 18 December 2024

3 min