Friday Jan 26 2024 11:42

9 min

Joe Biden wanted to talk stats yesterday. So let me give you some stats about the US economy, too. 3.3% growth in the final quarter – whoo yeah USA!! $2.581 trillion in new govt debt last year – interest payments now top $1tn …oops! Well it’s fiscal largesse to boost productivity and infrastructure, not layering on debt for future generations!! 25 states have signed a letter pledging their support to Texas and its constitutional right to defending the Southern Border. Bidenomics and radical leftist social policies come at a YUGE cost. Still markets don’t give a damn – the S&P 500 rose for a sixth day and a fresh record high. Markets are agnostic, but are they ignoring some major tail risks right now? The extreme tail risk right now is some kind of secession crisis between states like Texas and DC, and it looks less unlikely now than at any time since the Civil War. That is not to say it is ‘likely’, it is not, but it is not impossible and becomes more imaginable by the day.

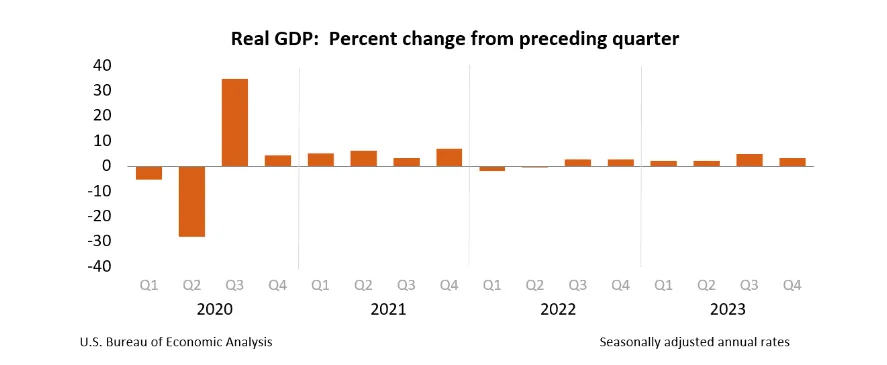

GDP at 3.3% in the final quarter vs 2.0% expected. Consumer spending remains very robust and government spending too – huge increase in debt last year of $2.5tn is hardly something that can be brushed aside as mere details.

GDP: ticking along on a debt train

So that headline growth number looks great, right. Here’s the BEA explaining that "the increase in the fourth quarter primarily reflected increases in consumer spending and exports. Imports, which are a subtraction in the calculation of GDP, increased." But it slowed from Q3, here is the BEA again noting “slowdowns in inventory investment, federal government spending, housing investment, and consumer spending. Imports decelerated." Expect Q1 ’24 to be weaker – inventories and trade are starting to act as headwinds.

Where did the Growth Come From?

What was the driver of this splendid, albeit slightly slower, growth? BEA: “The increase in consumer spending reflected increases in services (led by health care) and goods (led by recreational goods and vehicles).” Ok, so a load of boomers buying RVs and needing hospital treatment. Cool.And all those jobs, what about all the jobs that Biden has created? Let me show you two charts (I couldn’t overlay the two sets using FRED for some reason, but take a gander)

So ALL of the jobs created since 2019 have gone to foreign-born workers…funny how the Southern Border really really matters. now do you see why people will vote for Trump despite this ‘GREAT’ economy?

Meanwhile...

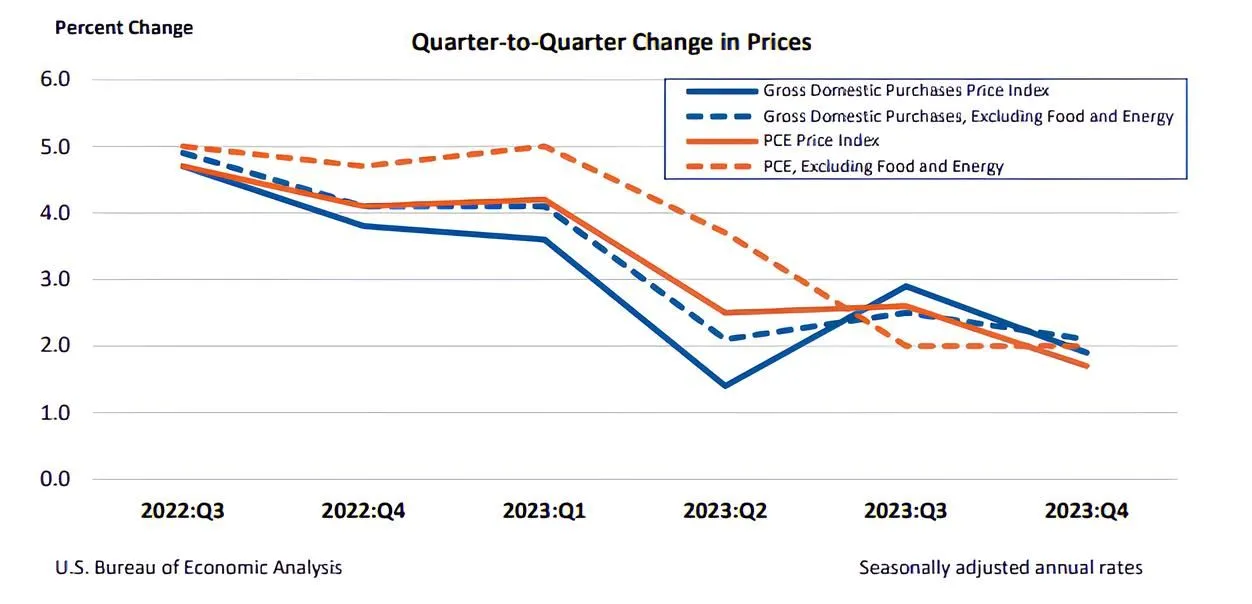

The Fed can look on with satisfaction to the inflation numbers the year ended with two quarters of core PCE inflation at an annualized rate of 2.0%, though over the year of course it was higher. Excluding food and energy prices, the PCE price index increased 4.1 percent, compared with an increase of 5.2 percent in 2022. But that second straight annualised 2.0% on the core PCE deflator is BIG – the Fed can say it’s guided the ship to a soft landing – its worry is what happens when it cuts; does inflation reaccelerate or has it done enough already?

2% ahoy – but the more accurate monthly figure is today and could start to get lumpy. The Fed will want to be absolutely certain of it before it starts cutting, which for some risks being too tight on the way out.

Everything on ice...but a March pivot may be coming. All policy rates remain on hold and the statement offered no clues about future policy moves. It was almost identical in content to the December statement. Markets are barely pricing in a move this spring – summer seems much more likely given the comments from Christine Lagarde and the uptick in inflation data in December. This meeting was always going to be a bit of a placeholder, but it did confirm that the ECB wants to be as data dependent as possible. On that front, unless inflation drops to 2% the ECB will remain on hold for as long as needed. The statement retained the line that “policy rates will be set at sufficiently restrictive levels for as long as necessary”.

But the presser from Lagarde and some hot US data did nudge things for EURUSD. Traders moved to price in 50bps of cuts by June, and 140bps of cuts by year-end from 130bps before the statement. That seemed to be on her failure to rule out a March cut...but that is the point of being data-dependent I suppose; you cannot rule anything out really. Bear in mind the move was within the range of the prior two days in the region of 1.0860-1.090...hardly major ructions.

And...sources were out on the wires after the meeting to say that the ECB is open to changing its tune – if not policy rates – in March. Lagarde though had stressed it was still too early to discuss rate cuts – what are they trying to get us to think? All told, it doesn’t alter my belief that the first cut is likely in June. But a change is coming – that could be good for German consumer sentiment, which plunged to -29.7 going into Feb.

Tags Directory

View allLatest

View all

Wednesday, 18 December 2024

3 min

Wednesday, 18 December 2024

4 min

Wednesday, 18 December 2024

4 min