Tuesday May 16 2023 10:13

7 min

Flat start to trade in Europe on Tuesday after another so-so session on Monday, stocks catching a little more bid as the morning progressed but no major moves. The DAX is flat, flat, flat not far off the year’s high; the FTSE 100 steady after it closed yesterday up 0.3% at 7,777.70. US futures are a bit light after a positive session on Wall Street on Monday. US 10yr rates steady just below 3.5%, the dollar is a bit lower, extending yesterday’s slip, oil flat after gaining yesterday with spot WTI to $71.50 and gold a little above $2k.

Data underwhelmed overnight. China industrial output, fixed asset investment and retail sales all came in below forecast, pointing to the recover losing momentum in April. Key test for sentiment today is the US retail sales figures. Estimates indicate a 0.7 per cent increase in overall retail sales from the previous month, following two months of declines. But Bank of America's "Consumer Checkpoint" data suggests slacker consumer spending, with total card spending per household declining -1.2% year-over-year. Excluding autos, core retail sales are seen +0.4% in April as against a -0.4% decline in March. Control Group for April seen at 0%, compared with March’s 0.3% decrease.

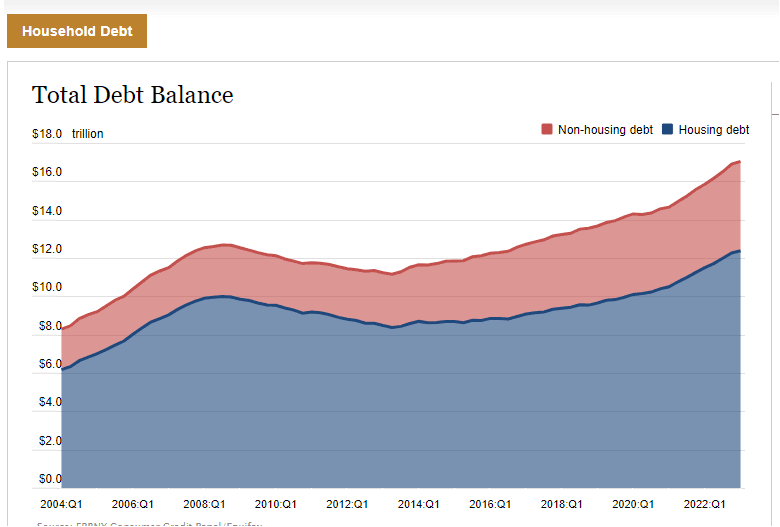

This is a key gut check for the US consumer – important for what the Fed thinks it can get away with. NY Fed data suggests American consumers are undeterred, with yesterday’s quarterly survey showing total household debt rose by 0.9% to a record $17.05 trillion, +$2.9 trillion higher than at the end of 2019.

This is fine

Paul Tudor Jones thinks the Fed is done with hiking rates, at a level that has historically slowed the economy and kicked off a recession, believes it could declare victory now. He thinks equity prices will go up this year even as the real economy could end up in recession...but also thinks Druckenmiller could be right that the S&P 500 is in a multi-year trading range with no gains for ten years. Both can be right.

Chicago Fed president Austan Goolsbee said the May hike was a close call and the effect of hikes is still in the mail. Atalanta Fed president Bostic (non-voter) added a bit more hawkishness to the discussion, noting that if there is a bias to action it would be to increase rates rather than cut.

The key question now is whether inflation stays down – no one thinks 2% is doable soon but if you can keep it at 3-4% you can stop. FactSet says a lot fewer companies are mentioning inflation on earnings calls...yes to less input inflation, but what about finished goods inflation and services? It’s the whole ‘greedflation’ story. Price might be a better word to look at.

Debt ceiling negotiations resume today – hopes of a resolution before the month is out apparently lifting Wall Street … but trading on fumes here within this dreadfully narrow range. Tech is showing a bit more momentum is crowded...Nasdaq up two-thirds of a percent.

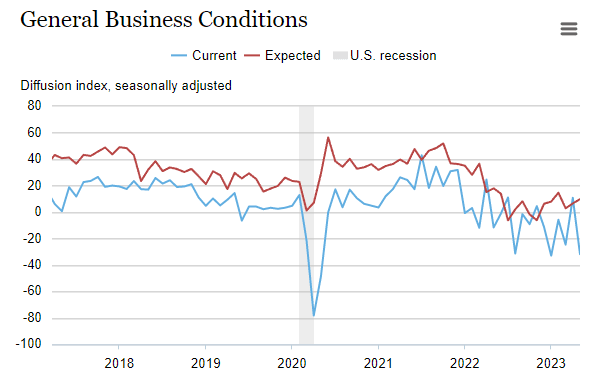

Empire State Manufacturing Survey was weak – the headline general business conditions index dropped forty-three points to -31.8. New orders and shipments plunged after rising significantly last month.

Vodafone shares sank 3% as it outlined plans to cut 11,000 jobs and forecast a €1.5bn decline in free cash flow this year. This has the look of a kitchen sink job from the new CEO Della Valle as earnings are weaker than expected as she gets to grip with this supertanker and tries to turn it around. It’s a bold move but investors will want to see what she does with Spain and Italy, selling these to focus on Germany and emerging markets, and reduce its debt, albeit this was down almost a fifth to ~£33bn. Group revenue increased by 0.3% to €45.7 billion, whilst adjusted earnings before nasties declined 1.3% to €14.7bn, both below analyst expectations. Management cited energy costs and a poor performance in Germany.

Imperial Brands first half profits up on price hikes...same old story. Robust pricing and aggregate market share up 20 basis points across its top-five combustible market portfolio, with next generation product (NGP) net revenue up 19.8%. Reported operating profits jumped 27%, with strong tobacco pricing +9.3%. Shares flat.

Land Securities portfolio down 7.7% amid warnings of ‘higher for longer’ rate environment...pre-tax loss of £622m, resulting from the £848m movement in the portfolio value. Underlying earnings rose 10%. Has the worst been discounted in commercial property? Shares rose 1.5% in early trade.

Greggs shares coming off a touch, down 1.5% with no upgrade to guidance, still +17% YTD. So far in 2023 it reported +17.1% like-for-like sales growth.

The dollar trades a bit weaker this morning after two strong days of gains that took it above the 50-day SMA, which is now offering the support.

GBPUSD – wage growth in the UK is not slowing...which is inflation positive. Hugs the trendline at 1.25 after rejection of the 1.2430 region. BoE chief economist Huw Pill says he might chosen different words to describe the decline in purchasing power. On rates he said "I'd like to think that we have done enough".

Tags Directory

View allLatest

View all

Thursday, 19 December 2024

3 min

Wednesday, 18 December 2024

3 min

Wednesday, 18 December 2024

4 min