Thursday Feb 9 2023 16:07

6 min

Rarely has there been such an obsession over what constitutes a recession. The US unexpectedly fell into a technical recession in early 2022 when there were two quarters of negative growth but then turned it around with positive GDP growth in the final two quarters, with Q4 GDP coming in at 2.9% on an annualised basis.

Or was it a recession in early 2022? The politicians were keen to point out that it most certainly was not, with the White House issuing a statement in July 2022 that “While some maintain that two consecutive quarters of falling real GDP constitute a recession, that is neither the official definition nor the way economists evaluate the state of the business cycle”. The Council of Economic Advisers went on to say that “The National Bureau of Economic Research (NBER) Business Cycle Dating Committee—the official recession scorekeeper—defines a recession as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months””. On that basis, the full year-on-year increase in US GDP of 2.1% sounds like it was all a storm in a teacup.

So why the ongoing obsession with recession?

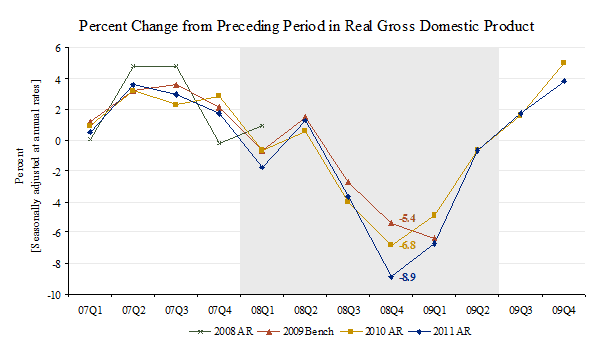

It’s not as if the GDP data itself is that useful at the best of times, given it is prone to revision. It took until August 2011 for the Bureau of Economic Analysis to admit that the financial crisis wiped even more off US growth than they thought, by a whole percentage point. From Q4 2007 until Q2 2009, US GDP cumulatively lost 5.1% rather than the prior estimate of 4.1%. On a quarterly basis the plunge looks even worse:

And that was a relatively “normal” recession where people lost jobs and consumers spent less. This time around we have a whole global lockdown to throw in, which caused deep swings in both supply and demand. On a micro level, consider Peloton. Suddenly everyone wanted one of their exercise bikes. The company tried to keep up with demand but supply chain issues made it difficult to step up production. Then the world re-opened, demand plummeted and the company was left with unwanted stock. Scale that up on an aggregate basis for the whole economy and you’re left with extreme volatility in the change in the whole economy’s inventories, as this blog post from former World Bank economist Frank Lysy shows:

In any case, is building up inventories more rapidly a “good thing”? What about running them down? What tells you about the health of the economy? The peculiarities of calculating GDP growth are a statistical quirk in normal times but the last three years have been far from normal.

Add in that GDP data is by its nature in the rear view mirror and you begin to wonder whether the recession obsession isn’t just a sign we are all losing our minds.

The GDP data is really all about the Fed. As much as the fundamental growth of the economy should impact the price of individual stocks, government bonds or credit spreads, the truth is that the price of money matters far more. If growth falters but investors expect the Fed to respond by cutting rates to zero, then the market falls back onto its Pavlovian reaction of buying risky assets. That’s been the story of the last 15 years so why should it be any different now?

Because of the small matter of inflation. When that gets going, the Fed can’t stop.

In 1994, Alan Greenspan’s Fed raised interest rates seven times in 13 months, doubling the effective Fed Funds rate. The peak of 6% came in February 1995. It didn’t go back down to where it began at 3% until the September 11th terrorist attacks in 2001, seven years later.

The failure of markets to accept high-for-longer will lead to even-higher-for-even-longer. The Fed’s Lorie Logan, who knows a thing or two about markets having previously run the QE portfolio at the New York Fed, warned that if financial markets don’t believe them, the Fed will have to raise rates further:

“We can and, if necessary, should adjust our overall policy strategy to keep financial conditions restrictive even as the pace slows. For example, a slower pace could reduce near-term interest rate uncertainty, which would mechanically ease financial conditions. But if that happens, we can offset the effect by gradually raising rates to a higher level than previously expected.”

The Fed’s Bostic gets the final word, or as he put it “three words: A Long Time”, when asked how long rates would be above 5%.

So it doesn’t really matter if there is a recession or not. The Fed is sticking to its guns. That means that even as growth slows, interest rates will remain high. That will lead to a less inverted US yield curve as rate cuts will be priced out, wider credit spreads and lower equity prices. The definition of a recession should be the least of the market’s worries.

Tags Directory

View allLatest

View all

Thursday, 19 December 2024

3 min

Wednesday, 18 December 2024

3 min

Wednesday, 18 December 2024

4 min